After NYMEX WTI climbed higher all last week, topping $90/Bbl, euro-zone worries yesterday caused a 4 percent fall in crude to close at $88.14/Bbl. That is a still a long way above estimates of $50/Bbl break-even prices for crude produced from Eagle Ford shale. Oil production in the Eagle Ford is now close to 600 MB/d and estimated by Bentek to rise to over 700 MB/d by the end of this year. This South Texas play is attracting producers like bees to a honey pot. Midstream infrastructure projects are springing up left right and center. In the first of a series we look at how Eagle Ford crude prices compare to the Bakken.

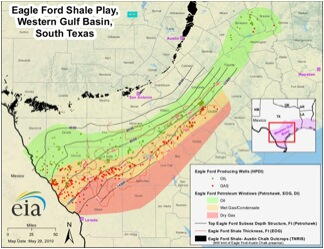

The Eagle Ford is a sedimentary shale rock formation stretching 400 miles from just northwest of Houston, to an area south of San Antonio and finally all the way to Mexico. The shale lies between 4000 and 14,000 feet below the surface. The formation has 3 windows (see map). To the north is the oil window, directly south of that is the "wet gas" window - high in natural gas liquids (NGL) and condensates, and further south, the dry gas window. Because of the high relative value of crude and NGLs versus natural gas, most of the current Eagle Ford drilling activity is in the northern part of the play. In this blog series we are focusing on crude oil and condensate production from the Eagle Ford. We covered the challenges of NGL production in the Eagle Ford earlier in the year (see “Lumpy – Soaking Wet – Moving Fast – That’s Eagle Ford NGLs”).

“Eagle Ford” sounds so gosh-darn-all-American that they might as well have named it Apple Pie. In fact it derives its name from the old town of Eagle Ford, now a neighborhood in West Dallas, where outcrops of the shale were first observed. As it happens, the current oil bonanza is located closer to San Antonio, 300 miles to the south of that old Eagle Ford neighborhood. Otherwise some bright spark in Hollywood might have justified resurrecting that thar 70’s TV show about oil barons in Dallas. Wait! They did that! http://www.ultimatedallas.com/

Compared to Bakken shale crude landlocked in North Dakota with limited takeaway capacity by pipeline, train and truck, a logjam at Cushing and tortuous paths to market on the East and Gulf Coasts, (see The Bakken Buck Starts Here Part I, Part II, Part III and Part IV) Eagle Ford is knocking on heaven’s door. Much of the crude production is located less than 100 miles from the Texas Gulf Coast – the world’s largest refining center with 16 MMB/d of capacity. The South Texas area is also crisscrossed with existing pipeline infrastructure that can and is being readily adapted to transport Eagle Ford production to market.

This fortunate locational advantage combines with some of the highest initial production rates of any US shale region to make Eagle Ford a beacon for producers. In the Eagle Ford, drilling depths are less and the shale fractures easier than Bakken shale. According to EOG Resources, Inc, Eagle Ford wells come in around $5.5 million while Bakken wells average over $8 million. New wells can take as little as 2-3 weeks to drill in the Eagle Ford. This July (2012) there were 251 working rigs in the Eagle Ford play compared with 182 a year ago.

Given all these advantages, how do the prices Eagle Ford producers realize for their crude compare to Bakken and WTI crude? To understand these differences we took a look at the prices being quoted by midstream crude aggregators such as Plains All American and Flint Hills Resources (part of Koch). The Plains posted prices for the first 6 months of 2012 (see Chart 1 on the left below) show an average $31.5/Bbl premium for Eagle Ford Crude (40-44.9 API) over North Dakota Williston Light Sweet (40-44.9 API). The Eagle Ford prices posted by Flint Hills this year so far are priced at an average $8.5/Bbl premium to WTI and have recently traded closer to light Louisiana sweet (LLS) the US Gulf light sweet benchmark (see Chart 2 on the right below). This is because sufficient takeaway capacity to deliver Eagle Ford crude to Houston has now become operational. We will detail the new takeaway capacity later in this blog series.